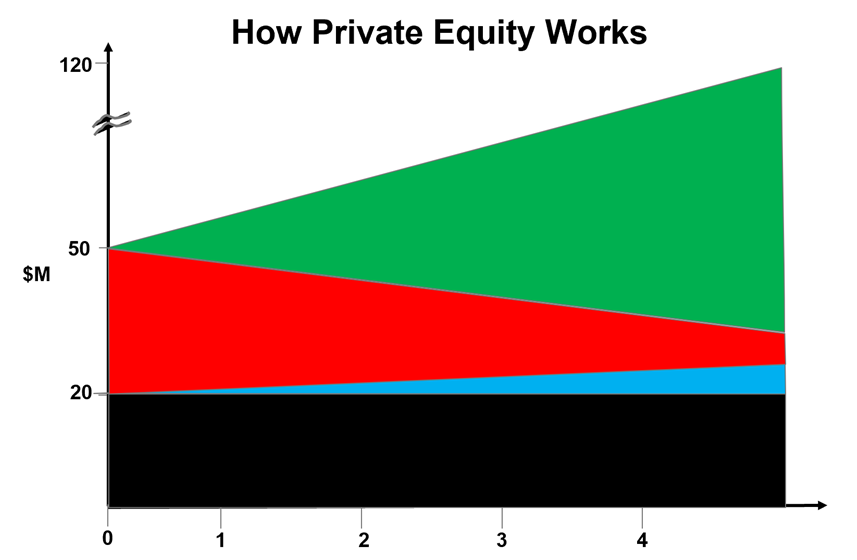

Tool

Summary

Below is excerpted from: The (Not So) New Game in Private Equity

By: Kerry D. Moynihan, Partner, Boyden Private Equity & Venture Capital

The origins of today’s private equity industry date to 1946 with the foundations of American Research & Development Corp. (ARDC) & J. H. Whitney. Prior, risk capital had almost exclusively been the domain of wealthy families. Venture capital pioneers Mayfield and Kleiner Perkins were founded in 1969 and 1972, respectively.

In the buyout realm, the origins of LBO pioneers KKR began at Bear Stearns with “bootstrap” investments in the early 1970s, forming the foundation of the firm as we know it today. TH Lee; Forstmann Little; Welsh, Carson, Anderson & Stowe; and GTCR were all in operation by 1980 and became major players.

The modern private equity business continued to emerge in the 1980s with the realization that there were major discrepancies between public company management interests, the age-old “agency problem” and the values that could be unleashed were business units to be decoupled from large public companies. The year 1980 saw some $2.5 billion raised dedicated to the emerging alternative asset class and in the decade that followed nearly $22 billion was raised by venture and buyout funds.

The wide availability of junk bond financing fuelled a boom during the 1980s, followed by a crash as the stock market tanked in October 1987. High yield financing, or “junk bonds,” dried up for a time, and Drexel Burnham, the leading purveyor of these instruments, later went down.

However, institutional investors had picked up on the higher returns available to PE than in the public markets. Key to these was the availability of debt financing, the disparity between management that were merely salaried and those that were incentivized by equity, and the discrepancy between public and private market information. For much of the next two decades, private equity vastly outperformed the public markets. Clearly, the emergence of technological innovation in software, semiconductors, and telecom fuelled the venture side, while widespread industry consolidation and globalization largely propelled the LBO market.

As ever more money flowed into pensions and other institutional investor funds, the demand for higher yields accelerated. This put more capital into the financial markets seeking higher returns and the boom continued. Of course, there were blips and shocks, including the Foreign Debt crisis of 1997/98, the bursting of the dotcom bubble around 2000, the cessation of normal market activity following the 9/11 attacks, and perhaps most seriously, the major Financial Crisis after the collapse of Lehman Brothers and Bear Stearns in 2008.

However, markets rebounded, time and time again. Institutional capital, which seems to have a short collective memory, always seeks ever-higher levels of Alpha (relative return) and will accommodate Beta (risk), often in unison, seemingly without independent, objective decisionmaking.