Most leadership teams know the problem.

They set an annual revenue target, build spending around it, and move forward as if the planned revenue inflow is already on its way. If revenue later develops more slowly than hoped, the organization is forced to pull back, delay hires, cut initiatives, and explain why the original plan no longer holds.

That is not disciplined planning. It is front-loading optimism and dealing with the consequences later.

A better approach is to let revenue lead expenses.

This starts with distinctions that are often blurred: the difference between the revenue goal, the revenue forecast, and the currently authorized level of spending.

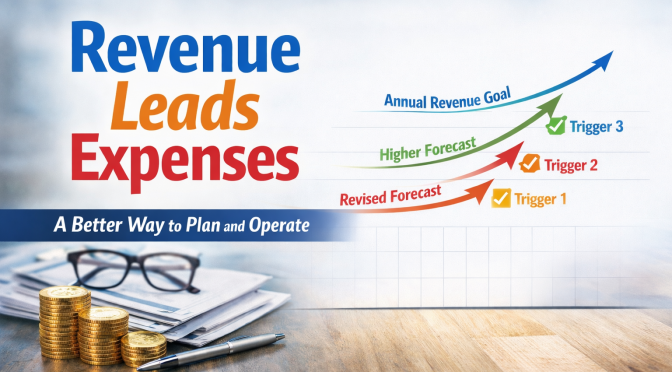

The revenue goal is the level of performance the organization intends to produce over the course of the year (with ~75% confidence). It sets direction, expresses ambition, and gives management and the team a target to drive toward. It is, by design, an expression of intent rather than a prediction, and it is set once for the performance period (e.g., a year).

The revenue forecast is management’s best current estimate of what is most likely to materialize based on facts known at the time. It is a high-confidence view (90+%), not an aspiration dressed up as a projection. In practice, teams should be able to articulate the confidence level behind the forecast, explain why it is defensible based on current evidence, and state clearly what must occur for it to materialize. It is established at the beginning of the performance period and updated continuously as new information becomes available.

The authorized expense level follows from the forecast. The organization may appropriately communicate an ambitious plan and budget externally, but it should not authorize spending internally at the full goal level from the outset simply because that is where it intends to end the year. Initial spending should be based on the revenue that management has high confidence will materialize. Spending should remain aligned with the forecast from then on.

A common approach is to spend at the goal level and then cut if triggers are missed. A better approach is for management to begin the year with a forecast-based level of spending. As the year unfolds and predefined triggers are met, the forecast may be revised upward. Each higher forecast then authorizes a higher level of spending.

Done well, this creates an effective operating rhythm. The organization expands deliberately as evidence improves. Spending rises as the facts justify it, with each step grounded in current performance and validated progress.

Note that the revenue leading expenses approach requires clarity about what counts as a trigger. The trigger might be a revenue milestone, a booking threshold, a conversion rate, a renewal event, a signed commitment, or another concrete indicator that the revenue outlook has strengthened. Management should define as part of its plan what justifies moving to a higher forecast and, therefore, a higher spend path.

The accompanying chart illustrates the logic connecting revenue leads to expenses. While the annual revenue goal remains fixed, the initial forecast establishes the baseline spending posture. As specific triggers are met, management adopts updated forecasts. Each revision builds upon the previously authorized path, supporting a higher level of cumulative spending.

This approach reinforces the discipline of aligning spending with current evidence rather than assumptions, helping leadership make decisions based on what is actually unfolding rather than what was originally planned. The discipline is as follows:

- Plan to the goal. Decide what the organization is trying to produce and what it would take to operate successfully at that level, even though not all of that spending is authorized on day one.

- Forecast what is most likely. Establish a higher-confidence view of the revenue expected to materialize based on current facts.

- Let the forecast in force define the current spend level. Authorize spending based on what management currently has high confidence will come in, not simply on what it hopes to produce.

- Raise authorized spending only as triggers are met and the forecast improves. Expand spending as evidence strengthens and the revenue outlook becomes more secure.

At any point in time, leadership should be able to answer three separate questions:

- What is the annual revenue goal?

- What is the current revenue forecast?

- What level of spending is now authorized based on that forecast?

Those answers should be connected, but they should not be assumed to be the same.

That is what it means to let revenue lead expenses. It is a way to stay ambitious without getting ahead of the facts.